Enerflex is a steal at this point. It started the year trading around $12 a share and has since fallen to around $6.50 as of the writing of this post. I recently bought some shares around this price. They have continued to be profitable amidst a formidable business climate. Low natural gas and other liquid fuel prices have rocked the energy industry this year all around the world. According to economic pundits everywhere, this is because of low temperatures and low demand due to COVID-19. Since Enerflex is engaged in the sales of equipment to the energy industry (mostly natural gas), you may expect that they should have realized massive losses. This has not been the case. Enerflex has seen its earnings reduced, but has not recorded any losses as of writing, which is phenomenal from my perspective. This shows that their margins are on point and that they are able to maintain some business due to their strong business connections worldwide. In 2021, I expect we will see energy prices trade slightly up as economies around the world begin the long recovery from COVID.

Looking at Enerflex from a revenue perspective, it really shines right now. Currently its revenue is about 2.35x its market cap (the value of all of the shares). This is the most impressive value indicator and really shows that the company has far more reach than the market is giving it credit for. The P/E is around 6.8 for the earnings from Q3-2019 to Q3-2020 (as the Q4 2020 earnings are not in yet).

Enerflex is a highly geographically diversified company. This is advantageous as it enables them to move into markets where demand for its services is increasing, and out of markets where it is decreasing. Natural gas should play a role in the transition from “dirty” sources of energy such as coal to fully green sources such as wind or solar. According to the CEO Mark Rossiter in his letter to shareholders, this is the strategy being implemented in “all 17 countries where (Enerflex) operate(s)”. Of course you can’t trust all the hype a CEO might throw at you about his company, but this point was interesting.

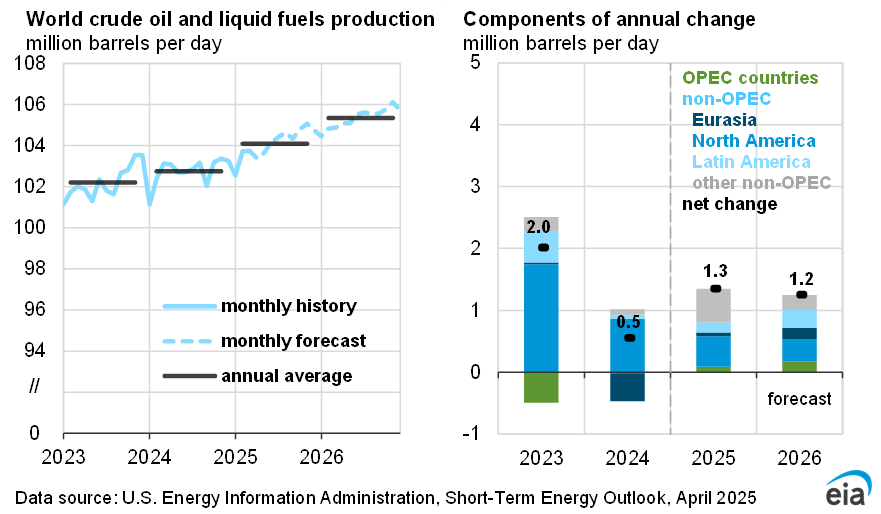

Natural gas is expected to trade moderately higher in 2021 compared to 2020. This is vital for the sustained success of Enerflex.

Consensus: This company is a buy at this price. There is certainly a lot more upside than downside. The biggest risk factor is continued weakness in fuel prices. If you are bullish on the energy sector, this is a good value pick.

{kind=link}

Great blog you have got here..

It’s difficult to find quality writing

like yours these days. I really appreciate people like you!

Take care!!

That is very kind of you to say, thank you.