MRG.UN is the ticker for Morguard North America Residential REIT. It’s a subdivision of the massive real estate company Morguard. MRG derives revenue from Canada and the USA from its 42 multi-residential properties. This number includes apartment communities as well as apartment buildings.

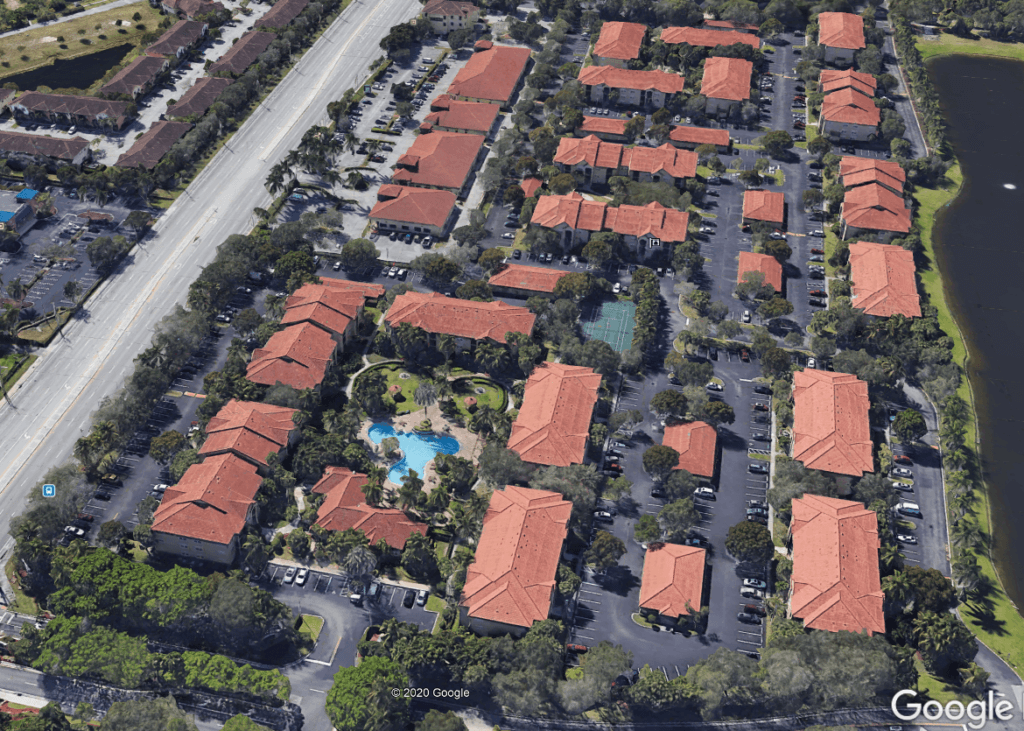

Below are two examples of what MRG.UN owns. Square 104 is a low/mid rise, whereas Barrett Walk is an “apartment community”. I recently bought some shares of Morguard REIT at around $15.90. In this post I am going to tell you the reasons why you should throw some love 💖 MRG’s way.

Square 104 – Edmonton

The Pros

Fundamentals & Relative Valuation

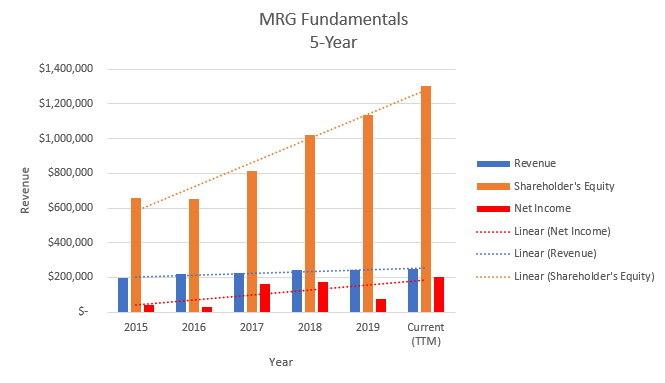

What I like about Morguard REIT (MRG.UN), and the reason that I call it a “sustainable powerhouse” is the fact that it just keeps chugging along. The COVID-19 pandemic didn’t even really slow it down all that much.

As you can see, the fundamentals have continued to perform well between 2019 and the year-to-date, yet the stock value has decreased. Obviously that’s a recipe for a discounted stock! I mean just look at that growth in shareholder’s equity. It has doubled since 2015 to the point where now every $16 dollar share of Morguard holds around $30 of shareholder equity. That puts the book value at ~.5. In addition, the growth in Net Income, albeit unpredictable, puts the shares at a 5x P/E ratio currently. Compare that to it’s five-year P/E average of 14.

The widely anticipated “cycling from tech into value stocks” anticipated to take place in 2021 could benefit MRG. Basically, pundits anticipate that people will begin to move their money out of the heights of technology and onto the firmer ground of value stocks. Is this going to happen for certain? Who knows. However, I think this scenario is likely and this is something which we are already seeing. Nobody wants to be at the top of a tech bubble when it comes crashing. People would rather sit in a value company and collect dividends… Speaking of which.

Dividends

MRG yields a 4% dividend. I anticipate people will come running to REIT dividends sometime soon. Why? Well, developed countries have reached historically low bond yields. If this trend continues it means more and more people will seek safe alternatives to bonds. A REIT like MRG fits that bill real nice. It has a beta of 1.03 – inline with the market as a whole. This makes it look like a stable, safe place to store money. It has a sustainable growth rate of around 15% – no need for excessive dilution. Evidently a lot of people, including me, don’t want to sit in a government bond and receive sub-1% annual interest. It just doesn’t work for me. How about you?

Life isn’t all candy canes and rainbows though. Below are the (not so) good things about MRG.UN.

The Cons

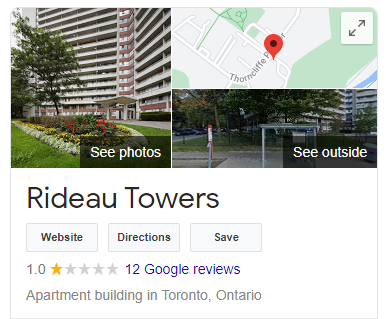

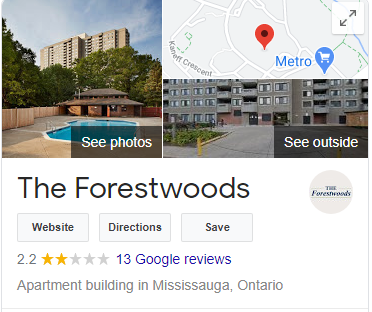

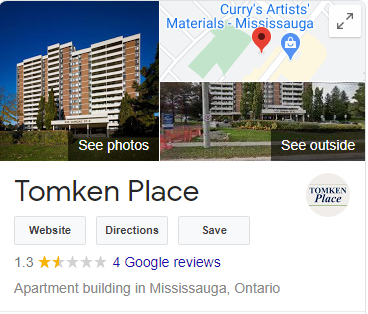

Building Ratings

What I don’t like are the ratings on some of Morguard NA’s buildings. Especially the ones in the GTA Canada area.

Hopefully Morguard can implement some sort of strategic initiative to fix these low ratings because they don’t bode well for their reputation. It’s really not what I want to see as an investor. We want ethical revenue – not just any revenue. In due time I think Morguard can make this happen. Their website is riddled with “initiatives” and “strategic plans”. They might want to consider making this one of them. “Project 5-Star 2025” or something.

Occasional Dilution

Fortunately this dilution is predictable. It looks like Morguard is diluting their shares every 2-years. And this year – 2021 – is a year they are skipping. Phew! When I say dilution, I am talking in the range of 10-15%. Again, not something that’s going to wipe out your investment. Just something to be wary of – especially come 2022.

The Conclusion

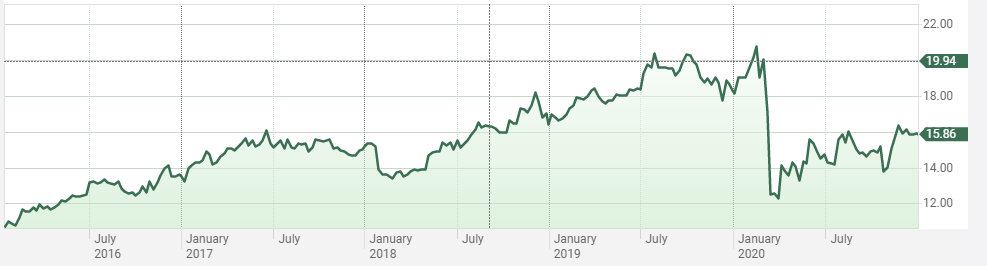

Buy. I would expect moderate 5-10% capital gains in 2021 coupled with the 4% dividend. If you can wait, I would try to get in below the current 16 dollar price. From what I can see on the stock price graph we may be at a local maximum. Take a look for yourself. Do some research for yourself.

Leave a comment and let me know what you think of MRG. And as always,

Happy Investing.