Archegos Capital Management was a company which few people had heard of before this year. Despite being a multi-billion dollar fund, it didn’t seem like it was of much consequence to anybody. That is because it was what is known as a “family office” – a fund set up to manage one family or individuals wealth. But this innocent perception was drastically altered when the firm collapsed under the weight of its leverage earlier this year, causing billions upon billions in losses.

Despite being a multi-billion dollar fund, it didn’t seem like it was of much consequence…

The news of the collapse of Archegos shocked the financial world when it happened in late March of this year. Numerous banks, notably Credit Suisse and Nomura, suffered highly material losses. But that is not where the damage stopped. Shareholders of various companies were negatively impacted by low share prices as banks tried to exit their positions.

Fortunately, Archegos was not quite large enough to cause a global financial meltdown. But, this whole case begs the question: What exactly is Archegos Capital Management?

Semi-Humble Origins

To understand where the Archegos money – a sum of about $10 billion dollars according to popular reporting – came from, we must go back. Back to 1996 in New York City, and to a man named Julian Robertson. Robertson ran the highly successful Tiger Fund at the time. He had grown Tiger into a nearly $8 Billion dollar enterprise by 1996.

It was also at this time that Robertson decided to hire Bill Hwang, then 32, as a financial analyst. Hwang’s job would thus be to sort through the numerous financial instruments up for sale and decide on the one’s worth buying.

Over the next five years, Hwang developed a close working relationship with Robertson. Along with some other employees at Tiger Fund, Hwang became a protégée of Robertson. He and these other protégées would become known as the Tiger Cubs.

By the time 2001 rolled around, Robertson had decided to shutter the doors on Tiger Fund and move on to other projects. He returned the funds money to its rightful owners, the investors, and closed up shop. Robertson decided to give some of the Tiger Cubs some money to start their very own funds.

After five years of extensive mentorship, Robertson felt that Hwang was ready to run his very own fund and gave him $25 Million to do just that. Hwang accepted this seed money and founded his own fund. He named it Tiger Asia Fund. Obviously this name referenced Robertson and Tiger Fund’s contribution to the fund, but it also referenced Hwang’s Asian business connections and heritage. Hwang was born in South Korea and moved to America as a boy. He also traded in Asian markets, specifically the Hong Kong stock exchange.

Tiger Asia Fund

Tiger Asia Fund was founded with the aforementioned $25 million from Robertson in 2001. Admittedly, little is known about what trades Tiger Asia made over the years.

What we do know is that it returned a cool 16% average annual return in its years of operation (2001-2012). This return would have been much higher were it not for large losses incurred in the financial crisis (circa 2008). Therefore, it is not at all surprising that investors were drawn to the fund, especially in the early years when it was making phenomenal returns. It is reported that Tiger Asia had billions in assets under management at a certain point.

We also know that, in 2012, the SEC charged Hwang with insider trading on Chinese bank stocks. Hwang had been given confidential information which he promised not to trade on. Then he decided to trade on it anyways. For this malfeasance, Hwang was ordered to pay a fine of $44 million to the SEC for this insider trading. Shortly thereafter, he shut down the fund and returned all outside capital to investors.

What is important to note is that Hwang made a lot of dough during his management of Tiger Asia Management, even after paying the fine.

Archegos Capital Management

After the insider trading saga Hwang was down, but not out. Not just yet. Hwang had amassed a significant personal fortune over the years of hedge funding. He decided to roll this money into a family firm called Archegos in 2013. As I mentioned earlier, Archegos only ever managed Hwang’s capital.

Because of this fact, securities regulators didn’t care that much about what Hwang was doing. It was his money after all. That was the thinking of regulators. This makes Archegos’ dealings quite murky. Even the banks which Hwang dealt with did not know where Hwang had all of his money tied up. After all, he dealt with many banks which do not share this information with each other.

“Bill Hwang is known as a bit of a cowboy. He runs a very concentrated, highly leveraged book.”

Thomas Hayes, Great Hill Capital, LLC

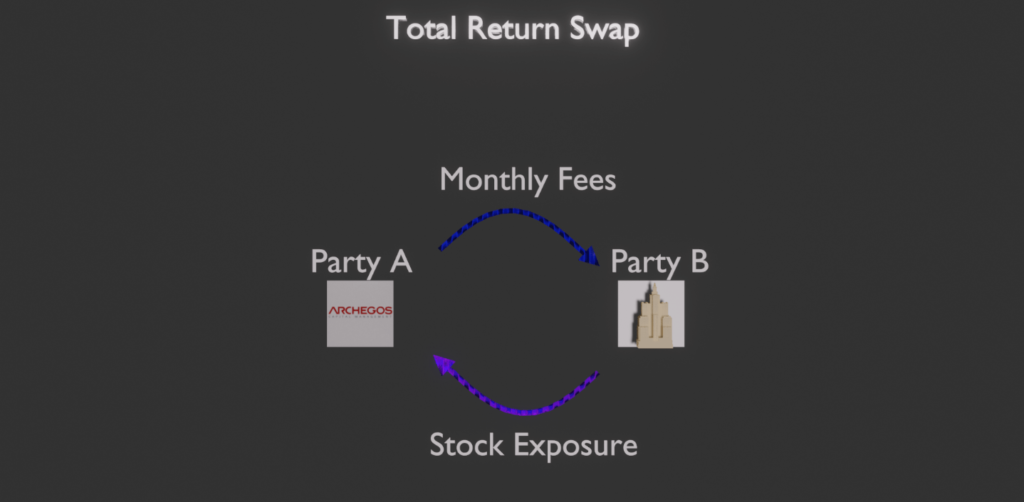

What is evident is that Hwang’s strategy was highly leveraged. Leverage in this context means the banks were loaning Hwang stocks and/or money. This leverage was crucial for the rise and fall of Archegos. One of Hwang’s favorite leveraged plays is known as a Total Return Swap.

As you can see above, Hwang was paying monthly fees to banks for exposure to the returns (and losses) of stocks. When the stocks rose, Hwang was paid. When they fell, he paid for the losses. This is a fairly standard trade. Specifically, Hwang was paying for exposure to ViacomCBS and Discovery Inc, among other companies.

The Collapse of Archegos

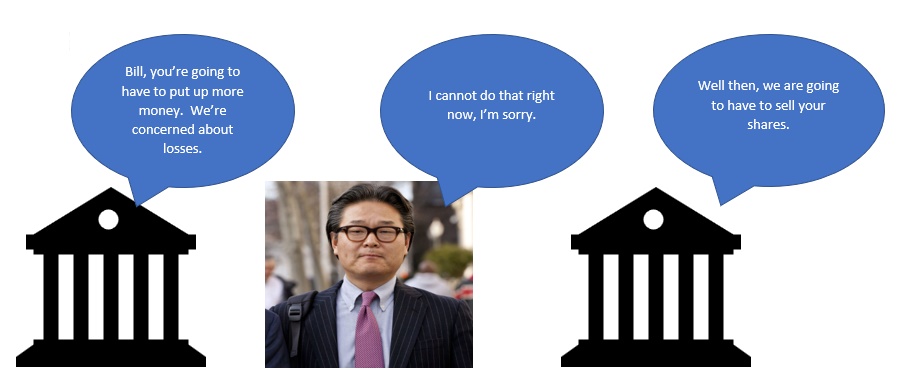

What went wrong in this case is that these stocks fell too much too quickly and Hwang could not cover these losses. Plain and simple. The banks began to liquidate positions, and the stocks fell more. Archegos lost everything and the banks lost big. All of this happened in a matter of days.

One of the major catalysts of the disaster was ViacomCBS. Hwang was apparently heavily invested in ViacomCBS via Total Return Swaps. When the shares began falling for unrelated reasons (fear of dilution), Hwang’s losses got out of control. The banks, concerned about losses, asked Hwang to put up more money to cover the losses. Since Hwang didn’t have more money, the banks started selling the shares to limit their losses. Things quickly got out of control.

As we know from economics class, price is determined by supply and demand. When the supply (because of bank selling) of these shares greatly outpaced demand, the price fell even more than it had already. This was the cause of the banks losses. And even though Archegos was obliged to pay for these losses (as per the Total Return Swap agreements), it did not have enough money to do so.

It should be noted that ViacomCBS was by no means the only company involved, though it was a major catalyst. Other companies which were sold off huge include Discovery Inc., Baidu, and Tencent. Archegos evidently held interest in these companies.

Why did the Banks lend Bill Hwang so Much?

Hwang’s phenomenal returns over the years had made him trusted in the eyes of the banks. They were willing to lend him multiples of what he could pay for, trusting in his investing skill and likely not knowing how leveraged he was elsewhere. This turned out to be a major error for all involved.

The Outcome

Many banks were impacted by this debacle. This article by FORTUNE magazine does a great job of outlining how different banks were involved. The biggest hit were Japanese bank Nomura and Swiss bank Credit Suisse.

Certain banks were able to act quickly to dispose of the shares they held. For instance, it has been reported that Morgan Stanley quietly disposed of $5 Billion in Archegos-linked shares the night before things hit the fan.

As for the star of the show Archegos, this is certainly game over.

In the end, it is important to manage risk. Big risks equal big returns and equally big losses.

Until next time,

don’t over leverage.